Impact

To boost credit affordability in India - apart from ease of use and adoption of credit, also aiding the mass transition from new to credit borrowers to experienced borrowers who understand loans have repayment obligations.

Debt-recovery is the hardest bottleneck for India’s credit growth right now, because we don’t have a compassionate and scalable solution for the borrower-distress across.

Currently when bank's give out loans and they go bad, it becomes a vicious cycle.

Banks, who are distressed by bad-debt, pressurize collection agencies.

Then these agencies in turn, apply pressure on the borrower, because they don’t have any other tools or data-driven strategies to operate with.

As a result, a borrower gets abused and threatened into repaying, despite genuine hardship and good-intent.

After listening to 2000+ collection-calls, sitting in NBFC call-centers for months and speaking 100s of borrowers, we have realized 1 important truth

"Borrowers who default aren't bad people. Their situations are"

But the current system just missed to acknowledge their good intent.

That’s when we decided to build a more patient and empathetic debt-counselling system - that is both - empathetic to the borrower, and efficient for banks.

Our approach doesn’t just nudge borrowers to pay, but it involves understanding each borrower’s POV, building trust, and helping them genuinely improve their place in the credit ecosystem.

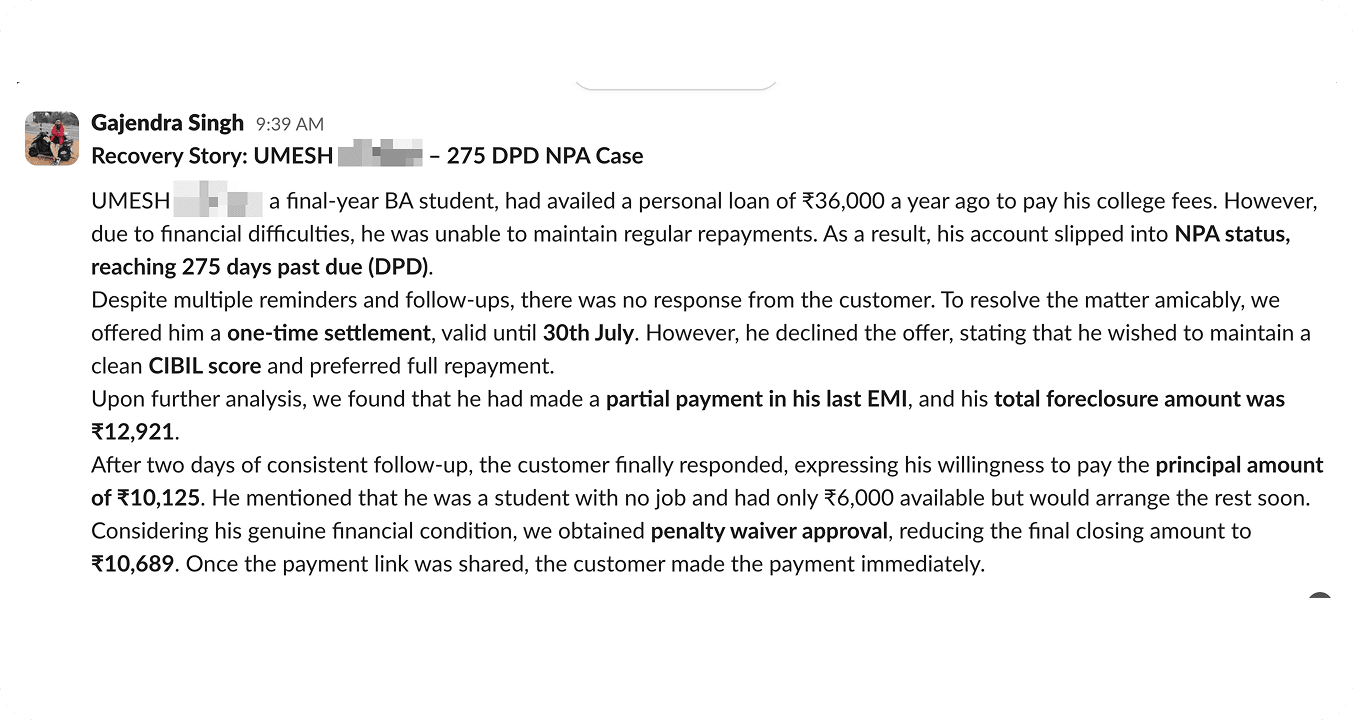

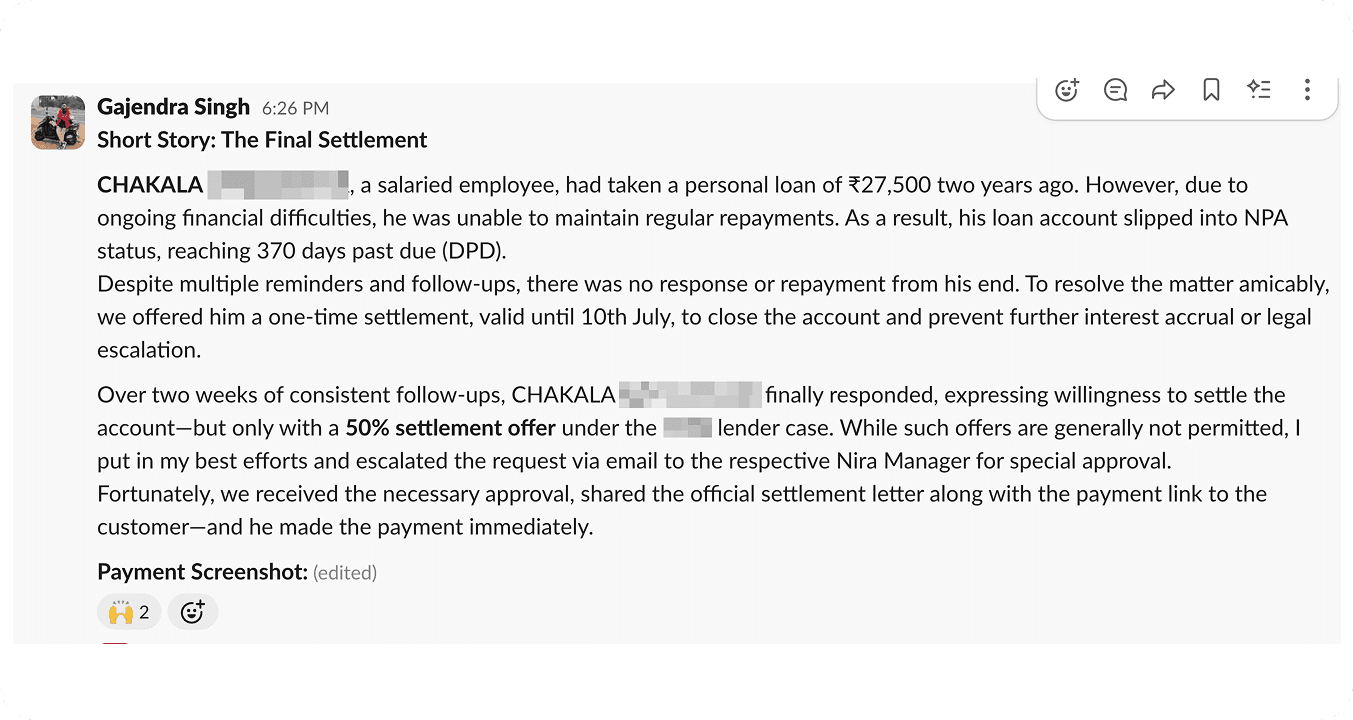

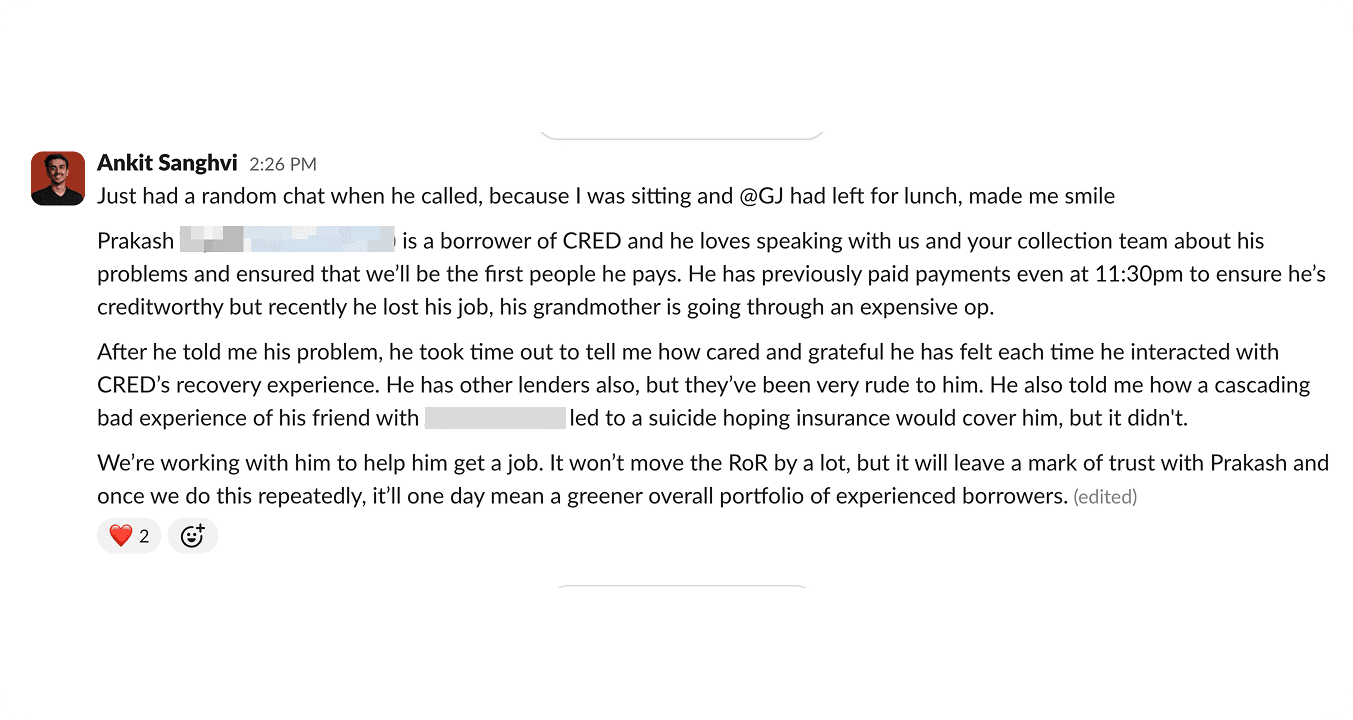

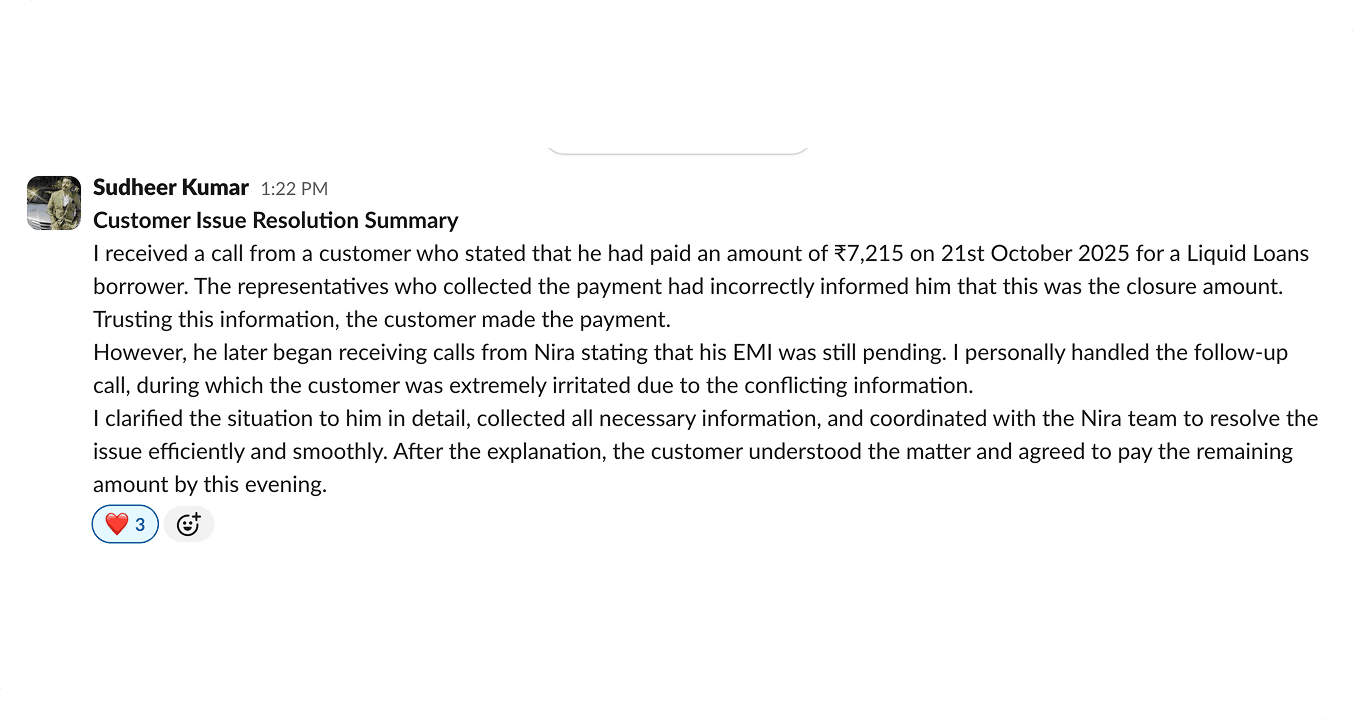

Below are a few real stories of impact. But if you're interested in the 10-year plan, read our manifesto