A 56-year-old textile-trader in Erode rang us last month. His business had slowed for two seasons, his ₹38 lakh property-backed loan slipped into NPA, and the bank had pasted a notice on his shop shutter that morning. He had thirteen days to "show cause" before the bank could take possession of the shop and the godown behind it.

The notice was issued under Section 13(2) of the SARFAESI Act, 2002. He had never heard of it. Most borrowers haven't until it's on their door.

Here is what SARFAESI actually is, what the stages look like, and what you can — and cannot — do at each one.

What SARFAESI is, in plain words:

SARFAESI stands for the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. It gives banks and NBFCs a fast-track legal route to recover dues from secured loans — home loans, loan-against-property, machinery loans, working-capital limits, gold loans above a threshold — without going to a civil court.

The trade-off the law made — the lender gets a faster process, the borrower gets specific procedural rights that must be used, on time, or lost.

The Act applies only to secured loans above ₹1 lakh with an NPA account (broadly, 90+ days overdue), held by a bank or RBI-registered NBFC. It does not apply to unsecured personal loans, credit cards, or agricultural land.

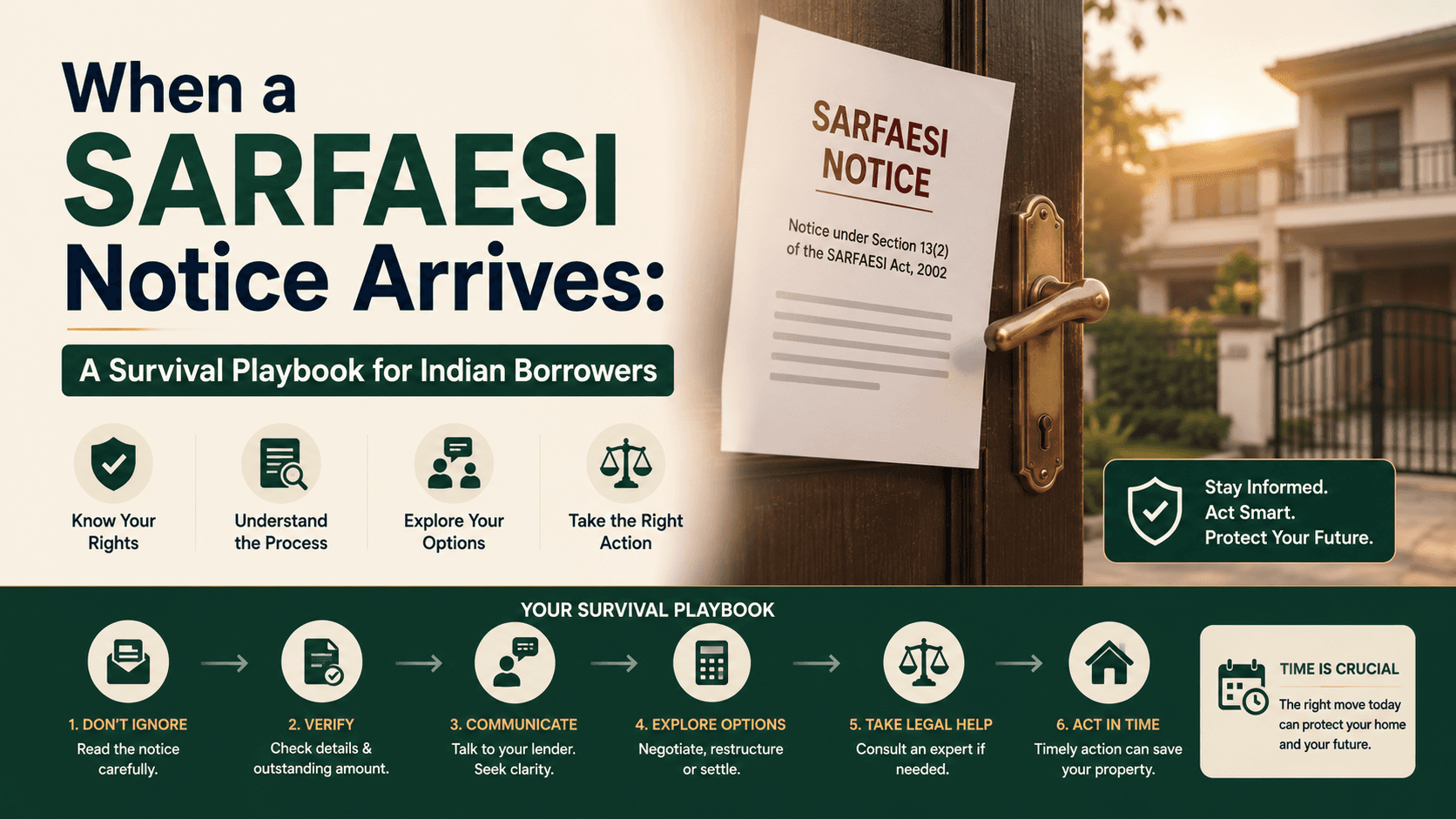

The five stages- and where you can act

Stage 1 : Account turns NPA. After 90 days of EMI default, the loan is internally classified as a non-performing asset. The bank will start sending reminder calls and letters. This is the cheapest stage to fix it. Approach the recovery desk now with a hardship letter and a restructuring proposal.

Stage 2 : Section 13(2) notice (60-day notice). The bank serves a formal demand letter stating the amount due and giving 60 days to pay or settle. During this window — you can make written representations objecting to the amount, the classification, or the procedure; the bank is legally bound to respond within 15 days; you can negotiate a one-time settlement, which banks often agree to at this stage to avoid a costly Stage 3 process; and if the loan is genuinely heading nowhere, you can voluntarily sell the property at market price and clear the dues. A voluntary sale usually fetches a far better price than auction.

Stage 3 : Section 13(4) possession notice. If the 60 days pass without settlement, the bank can issue a possession notice and physically take the property — either symbolic possession (paperwork only, you remain inside) or actual possession (the chief metropolitan magistrate orders you out under Section 14). You have 45 days to appeal to the Debt Recovery Tribunal (DRT) under Section 17. There is a DRT bench in Chennai and one in Madurai for Tamil Nadu cases. The DRT can stay the possession if there is a procedural error or genuine grievance. An appeal needs only the appeal fee, not a deposit.

Stage 4 : Auction notice. The bank publishes a sale notice in at least two newspapers (one English, one vernacular) giving 30 days before auction. You can pay the dues until the actual auction starts — the right of redemption survives until the property is sold. You can bring a private buyer to the bank at the reserve price, which is sometimes accepted. You can bid at the auction yourself (or through a family member) to buy back.

Stage 5 : Sale and confirmation. Once the property is sold, the bank applies the proceeds to dues. Any surplus after fees and interest is returned to the borrower. Any shortfall, the bank can pursue you for through the DRT.

What you should never do during SARFAESI

Ignore the notice. Every right you have under the Act is time-bound. Miss the window, lose the right.

Stop replying because you cannot pay the full amount. Your written representation under Section 13(3A) preserves your DRT appeal rights even if you cannot settle yet.

Sign a settlement letter that does not say 'full and final discharge of all dues, with no further claims and no legal action'. Anything less, and the bank can come after you again for the deficit.

Try to remove assets from the property after the 13(4) notice. This is a criminal offence under Section 29 of the Act.

When a lawyer is non-negotiable

For most borrowers, settlement and restructuring conversations don't need a lawyer. SARFAESI is the one situation that does. Every district in Tamil Nadu has a District Legal Services Authority (DLSA) that provides free legal aid to eligible borrowers, including SARFAESI representation. Many DRT advocates in Chennai and Madurai also handle the first consultation for a token fee.

The bottom line. SARFAESI gives the bank speed. It gives you windows. The borrowers who walk through this least scarred are the ones who replied to the very first letter - and the ones who waited for the auction notice to "see what happens" rarely got the chance to act.

A 56-year-old textile-trader in Erode rang us last month. His business had slowed for two seasons, his ₹38 lakh property-backed loan slipped into NPA, and the bank had pasted a notice on his shop shutter that morning. He had thirteen days to "show cause" before the bank could take possession of the shop and the godown behind it.

The notice was issued under Section 13(2) of the SARFAESI Act, 2002. He had never heard of it. Most borrowers haven't until it's on their door.

Here is what SARFAESI actually is, what the stages look like, and what you can — and cannot — do at each one.

What SARFAESI is, in plain words:

SARFAESI stands for the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. It gives banks and NBFCs a fast-track legal route to recover dues from secured loans — home loans, loan-against-property, machinery loans, working-capital limits, gold loans above a threshold — without going to a civil court.

The trade-off the law made — the lender gets a faster process, the borrower gets specific procedural rights that must be used, on time, or lost.

The Act applies only to secured loans above ₹1 lakh with an NPA account (broadly, 90+ days overdue), held by a bank or RBI-registered NBFC. It does not apply to unsecured personal loans, credit cards, or agricultural land.

The five stages- and where you can act

Stage 1 : Account turns NPA. After 90 days of EMI default, the loan is internally classified as a non-performing asset. The bank will start sending reminder calls and letters. This is the cheapest stage to fix it. Approach the recovery desk now with a hardship letter and a restructuring proposal.

Stage 2 : Section 13(2) notice (60-day notice). The bank serves a formal demand letter stating the amount due and giving 60 days to pay or settle. During this window — you can make written representations objecting to the amount, the classification, or the procedure; the bank is legally bound to respond within 15 days; you can negotiate a one-time settlement, which banks often agree to at this stage to avoid a costly Stage 3 process; and if the loan is genuinely heading nowhere, you can voluntarily sell the property at market price and clear the dues. A voluntary sale usually fetches a far better price than auction.

Stage 3 : Section 13(4) possession notice. If the 60 days pass without settlement, the bank can issue a possession notice and physically take the property — either symbolic possession (paperwork only, you remain inside) or actual possession (the chief metropolitan magistrate orders you out under Section 14). You have 45 days to appeal to the Debt Recovery Tribunal (DRT) under Section 17. There is a DRT bench in Chennai and one in Madurai for Tamil Nadu cases. The DRT can stay the possession if there is a procedural error or genuine grievance. An appeal needs only the appeal fee, not a deposit.

Stage 4 : Auction notice. The bank publishes a sale notice in at least two newspapers (one English, one vernacular) giving 30 days before auction. You can pay the dues until the actual auction starts — the right of redemption survives until the property is sold. You can bring a private buyer to the bank at the reserve price, which is sometimes accepted. You can bid at the auction yourself (or through a family member) to buy back.

Stage 5 : Sale and confirmation. Once the property is sold, the bank applies the proceeds to dues. Any surplus after fees and interest is returned to the borrower. Any shortfall, the bank can pursue you for through the DRT.

What you should never do during SARFAESI

Ignore the notice. Every right you have under the Act is time-bound. Miss the window, lose the right.

Stop replying because you cannot pay the full amount. Your written representation under Section 13(3A) preserves your DRT appeal rights even if you cannot settle yet.

Sign a settlement letter that does not say 'full and final discharge of all dues, with no further claims and no legal action'. Anything less, and the bank can come after you again for the deficit.

Try to remove assets from the property after the 13(4) notice. This is a criminal offence under Section 29 of the Act.

When a lawyer is non-negotiable

For most borrowers, settlement and restructuring conversations don't need a lawyer. SARFAESI is the one situation that does. Every district in Tamil Nadu has a District Legal Services Authority (DLSA) that provides free legal aid to eligible borrowers, including SARFAESI representation. Many DRT advocates in Chennai and Madurai also handle the first consultation for a token fee.

The bottom line. SARFAESI gives the bank speed. It gives you windows. The borrowers who walk through this least scarred are the ones who replied to the very first letter - and the ones who waited for the auction notice to "see what happens" rarely got the chance to act.