A 29-year-old salesperson in Anna Nagar, Chennai bought a ₹62,000 smartphone on a major e-commerce site last month. At checkout, three payment options appeared. The one labelled "No-Cost EMI - 6 months, no interest, no extra charges" looked obviously best. Six monthly payments of about ₹10,333. No interest. No hidden fees. He tapped it without reading the fine print.

Three things happened that he did not know about at the moment of tap.

First, the same phone, on the same site, was eligible for a cash discount that disappeared the moment he chose the EMI option. Second, a processing fee was added to the first instalment. Third, the full ₹62,000 was blocked against his credit-card limit, pushing his utilisation ratio sharply higher — which surfaced two months later when he applied for a home loan and was repriced at a slightly higher rate than he otherwise would have been.

Net effective cost of his "no-cost" EMI — meaningfully above the cash price. The label was accurate in one narrow sense and misleading in three larger ones.

This is not a story about a bad product. No-cost EMI is one of the more elegantly designed convenience products in Indian consumer finance. It is, however, a story about a label that the Reserve Bank of India has formally objected to for over a decade. Here is what is actually happening when you tap that button.

What the RBI said in 2013, and why it still matters?

On 17 September 2013, the Reserve Bank of India issued a circular (Notification Ref RBI/2013-14/238 / DBOD.No.FSD.BC.69/24.01.001/2013-14) directing scheduled commercial banks to discontinue "0% interest rate" schemes for consumer durables. The circular contains the relevant principle in plain language:

"The very concept of zero per cent interest is non-existent and fair practice demands that the processing charge and interest charged should be kept uniform product / segment wise, irrespective of the sourcing channel… In such loan products… the interest element is often camouflaged and passed on to the customer in the form of processing fee."

The circular went on to flag the practice as distorting the interest-rate structure and undermining pricing transparency. The RBI's underlying concern was that consumers cannot make informed decisions when the cost of credit is hidden inside a discount that they forgo, a processing fee they don't read, or a price uplift they don't notice.

In the years since, no-cost EMI schemes have evolved. Many today route through NBFCs rather than banks; some are structured as merchant-funded subventions rather than camouflaged interest. The form has changed. The RBI's underlying transparency concern has not.

For the consumer, what this means is simple - the regulator has been on record for over a decade that this label deserves scrutiny. That alone is reason to look behind it.

What "no-cost EMI" actually is

A no-cost EMI is not an interest-free loan. It is an arrangement in which the interest you would have paid is structured to be absorbed elsewhere - either by the seller (through a forgone discount), by the manufacturer (through a brand-subvention payment), or by both. The label is technically accurate in the narrow sense that the lender does not charge the borrower a separately itemised interest line. The cost has not disappeared. It has been relocated.

There are three places it is relocated to.

The forgone cash discount. Almost every product sold on no-cost EMI is also sold for cash, and the cash price is usually lower. The difference between the cash price and the EMI price is the implicit interest. It is not labelled as interest. It is, mathematically, exactly that.

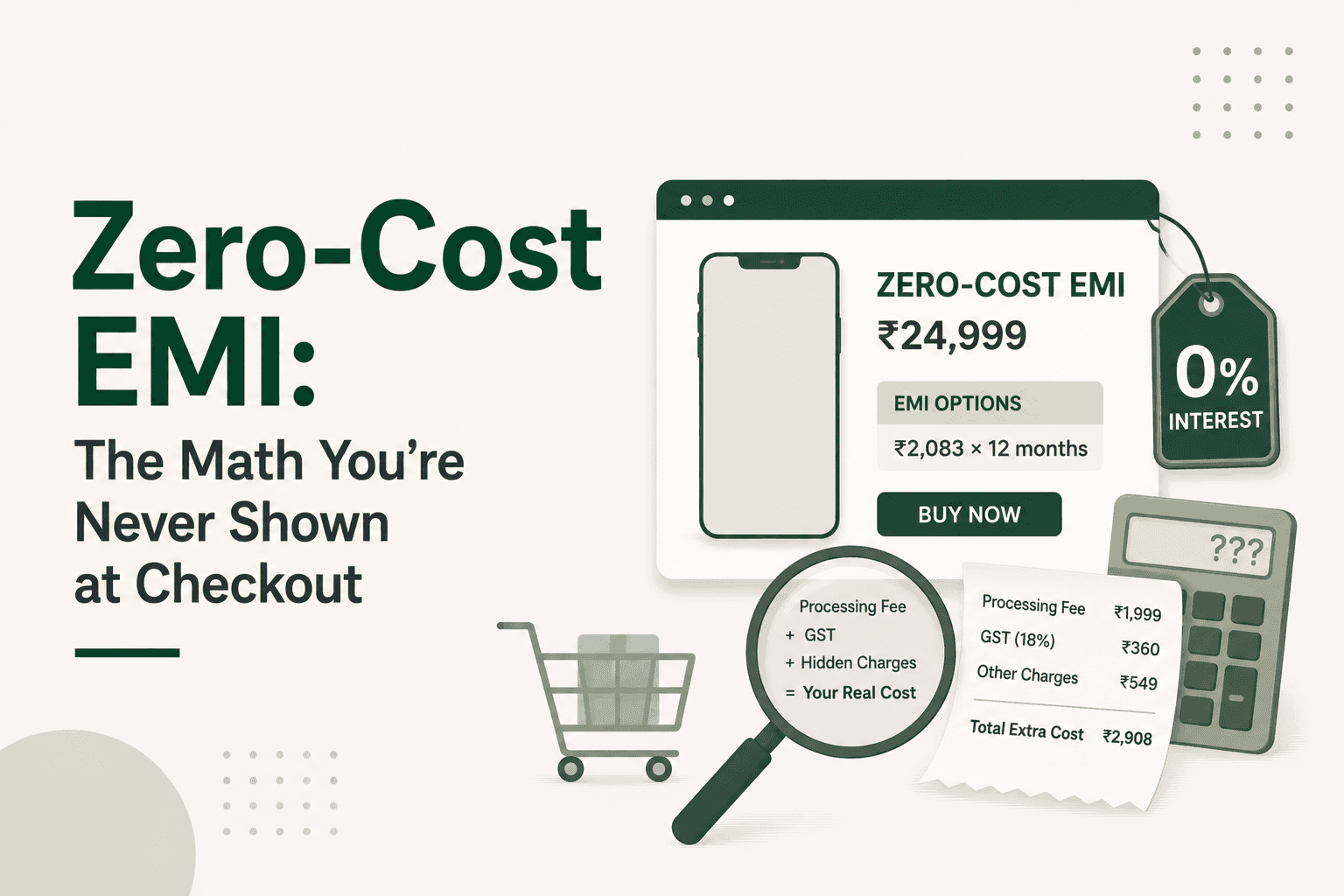

Processing and convenience fees. The lender (typically a bank or NBFC partnered with the e-commerce site) charges a one-time processing fee. This is usually small- ₹99 to ₹399, but it is a real cost added to the first instalment. This is the exact line item the RBI's 2013 circular flagged as a camouflaged interest charge.

GST on the implicit interest. Under prevailing tax practice, GST at 18% is levied on the financing component of these schemes- that is, on the amount the bank or NBFC is effectively financing for the buyer. This appears quietly on the invoice. Most buyers never notice it. The amount is small (₹200–₹600 on a ₹60,000 transaction), but it is a real out-of-pocket cost.

Together, these three usually amount to 4–10% of the headline price. On a ₹60,000 product, the effective premium is ₹2,500–₹6,000. The savings from the "no-cost" claim are real but smaller than the marketing implies.

The fourth cost that almost nobody talks about

Beyond the three visible costs, there is a fourth: the credit-utilisation impact.

When you book a no-cost EMI on a credit card (which is how almost all of these schemes work), the full purchase amount is blocked against your credit limit on the day of purchase. It is released back to your available limit only as each monthly instalment is paid down. For a ₹60,000 purchase on a ₹1 lakh credit limit, your utilisation jumps from whatever it was (say 20%) to 80% on day one, and only steps down by one-sixth every month.

The credit-bureau scoring model penalises sustained high utilisation. A utilisation jump from a low level to a high level for even one billing cycle typically reduces your credit score by tens of points- the exact reduction depends on your full credit profile, but the direction is consistent. For a borrower planning a home loan, a car loan, or any other major credit application within the next 6 months, this is often the largest hidden cost of the no-cost EMI. The interest math fades next to the score math.

The honest comparison, in three numbers

The cleanest way to evaluate a no-cost EMI offer is to compute three numbers at checkout.

Number 1: the cash price. Open a private or incognito browser tab. Look up the same product. Find the cash price (or the cash discount available on the same site). The gap between this and the EMI price is the implicit interest.

Number 2: the processing fee and GST. Look for "convenience fee," "processing fee," or "EMI fee" in the cart summary. Look for the GST line on the financing component. Read the EMI agreement before tapping confirm.

Number 3: the utilisation impact. Mental math - what is your current credit-card limit, what is your current outstanding, and how would this purchase push your utilisation ratio? If the answer is "above 50%," and you have any planned credit application in the next six months, the EMI is materially more expensive than it looks.

The sum gives you the honest cost of the EMI. Compare it to the cash price. The decision becomes mechanical.

When no-cost EMI is genuinely the right choice?

We are not arguing against the product. There are three situations in which it is the right call.

When the purchase is genuinely necessary, and a lump-sum payment would deplete the emergency fund. Liquidity preservation has value. Paying a small premium to keep ₹60,000 of emergency cash available is often the right trade.

When the realistic alternative is a credit-card revolve. If you would otherwise leave the purchase on a credit card and pay only the minimum due, the no-cost EMI at an effective annualised cost in the low double digits is dramatically cheaper than a 36-42% revolve.

When the seller's cash discount on the product is actually small or zero. Some sellers price the cash and the EMI similarly, especially during festival sales where the brand absorbs the financing cost. In those cases, the no-cost EMI is genuinely close to costless. The only way to know is to check the cash price.

When it is the wrong choice?

Three situations to walk away.

When you would not buy the product at the cash price. This is the most important filter. The EMI structure is designed to lower the perceived price of the purchase decision. If you would not pay ₹62,000 in cash for the phone, you should not be paying ₹62,000 on EMI for it either. The decision is the same decision; the EMI is just slower.

When you already have a credit-card outstanding being revolved. Adding another large block of credit on a card whose outstanding is not being cleared turns a manageable situation into a credit-score event.

When a major loan application is planned in the next six months. Home loan, car loan, education loan - these are repriced by the new lender on the basis of your current credit score. A utilisation-driven score hit at the wrong moment is more expensive than the entire EMI saving in the first place.

A practical checklist for the next purchase

The next time you reach a checkout page with a no-cost EMI option, run this in under sixty seconds.

Open the same product in a private tab. Note the cash price.

Add the EMI price + processing fee + GST on the financing component. Subtract the cash price. That number is the premium.

Check your credit-card limit and current outstanding. If this purchase pushes utilisation above 50%, pause.

Ask yourself, would I buy this at the cash price? If no, walk away regardless of the EMI option.

If yes to (4), and the premium in (2) is under 5% of the cash price, and the utilisation check in (3) is comfortable- tap with full awareness.

The checklist is what separates the borrower who used no-cost EMI well from the one who discovered, four months later, that they were paying for a convenience they did not need at a price they did not see.

The bottom line. No-cost EMI is a clever, well-designed Indian consumer-finance product. It is not free- the RBI said so explicitly in 2013, and the underlying principle has not changed. It is also not predatory. It is a structured premium charged to buyers who do not check the cash price. The single sixty-second habit of opening the same product in a private tab before tapping checkout ,that one habit captures most of what is recoverable from the trade.

This article is for educational purposes only and does not constitute financial, legal, tax or investment advice. Specific facts vary by case. For credit and loan-related decisions, work directly with an RBI-regulated lender or an RBI-recognised credit counsellor. For investment decisions, consult a SEBI-registered investment adviser. For insurance decisions, consult an IRDAI-registered intermediary. Statutes, RBI circulars and survey data referenced are accurate as of June 2026 and may be amended or superseded later- always verify with the primary source before acting.

A 29-year-old salesperson in Anna Nagar, Chennai bought a ₹62,000 smartphone on a major e-commerce site last month. At checkout, three payment options appeared. The one labelled "No-Cost EMI - 6 months, no interest, no extra charges" looked obviously best. Six monthly payments of about ₹10,333. No interest. No hidden fees. He tapped it without reading the fine print.

Three things happened that he did not know about at the moment of tap.

First, the same phone, on the same site, was eligible for a cash discount that disappeared the moment he chose the EMI option. Second, a processing fee was added to the first instalment. Third, the full ₹62,000 was blocked against his credit-card limit, pushing his utilisation ratio sharply higher — which surfaced two months later when he applied for a home loan and was repriced at a slightly higher rate than he otherwise would have been.

Net effective cost of his "no-cost" EMI — meaningfully above the cash price. The label was accurate in one narrow sense and misleading in three larger ones.

This is not a story about a bad product. No-cost EMI is one of the more elegantly designed convenience products in Indian consumer finance. It is, however, a story about a label that the Reserve Bank of India has formally objected to for over a decade. Here is what is actually happening when you tap that button.

What the RBI said in 2013, and why it still matters?

On 17 September 2013, the Reserve Bank of India issued a circular (Notification Ref RBI/2013-14/238 / DBOD.No.FSD.BC.69/24.01.001/2013-14) directing scheduled commercial banks to discontinue "0% interest rate" schemes for consumer durables. The circular contains the relevant principle in plain language:

"The very concept of zero per cent interest is non-existent and fair practice demands that the processing charge and interest charged should be kept uniform product / segment wise, irrespective of the sourcing channel… In such loan products… the interest element is often camouflaged and passed on to the customer in the form of processing fee."

The circular went on to flag the practice as distorting the interest-rate structure and undermining pricing transparency. The RBI's underlying concern was that consumers cannot make informed decisions when the cost of credit is hidden inside a discount that they forgo, a processing fee they don't read, or a price uplift they don't notice.

In the years since, no-cost EMI schemes have evolved. Many today route through NBFCs rather than banks; some are structured as merchant-funded subventions rather than camouflaged interest. The form has changed. The RBI's underlying transparency concern has not.

For the consumer, what this means is simple - the regulator has been on record for over a decade that this label deserves scrutiny. That alone is reason to look behind it.

What "no-cost EMI" actually is

A no-cost EMI is not an interest-free loan. It is an arrangement in which the interest you would have paid is structured to be absorbed elsewhere - either by the seller (through a forgone discount), by the manufacturer (through a brand-subvention payment), or by both. The label is technically accurate in the narrow sense that the lender does not charge the borrower a separately itemised interest line. The cost has not disappeared. It has been relocated.

There are three places it is relocated to.

The forgone cash discount. Almost every product sold on no-cost EMI is also sold for cash, and the cash price is usually lower. The difference between the cash price and the EMI price is the implicit interest. It is not labelled as interest. It is, mathematically, exactly that.

Processing and convenience fees. The lender (typically a bank or NBFC partnered with the e-commerce site) charges a one-time processing fee. This is usually small- ₹99 to ₹399, but it is a real cost added to the first instalment. This is the exact line item the RBI's 2013 circular flagged as a camouflaged interest charge.

GST on the implicit interest. Under prevailing tax practice, GST at 18% is levied on the financing component of these schemes- that is, on the amount the bank or NBFC is effectively financing for the buyer. This appears quietly on the invoice. Most buyers never notice it. The amount is small (₹200–₹600 on a ₹60,000 transaction), but it is a real out-of-pocket cost.

Together, these three usually amount to 4–10% of the headline price. On a ₹60,000 product, the effective premium is ₹2,500–₹6,000. The savings from the "no-cost" claim are real but smaller than the marketing implies.

The fourth cost that almost nobody talks about

Beyond the three visible costs, there is a fourth: the credit-utilisation impact.

When you book a no-cost EMI on a credit card (which is how almost all of these schemes work), the full purchase amount is blocked against your credit limit on the day of purchase. It is released back to your available limit only as each monthly instalment is paid down. For a ₹60,000 purchase on a ₹1 lakh credit limit, your utilisation jumps from whatever it was (say 20%) to 80% on day one, and only steps down by one-sixth every month.

The credit-bureau scoring model penalises sustained high utilisation. A utilisation jump from a low level to a high level for even one billing cycle typically reduces your credit score by tens of points- the exact reduction depends on your full credit profile, but the direction is consistent. For a borrower planning a home loan, a car loan, or any other major credit application within the next 6 months, this is often the largest hidden cost of the no-cost EMI. The interest math fades next to the score math.

The honest comparison, in three numbers

The cleanest way to evaluate a no-cost EMI offer is to compute three numbers at checkout.

Number 1: the cash price. Open a private or incognito browser tab. Look up the same product. Find the cash price (or the cash discount available on the same site). The gap between this and the EMI price is the implicit interest.

Number 2: the processing fee and GST. Look for "convenience fee," "processing fee," or "EMI fee" in the cart summary. Look for the GST line on the financing component. Read the EMI agreement before tapping confirm.

Number 3: the utilisation impact. Mental math - what is your current credit-card limit, what is your current outstanding, and how would this purchase push your utilisation ratio? If the answer is "above 50%," and you have any planned credit application in the next six months, the EMI is materially more expensive than it looks.

The sum gives you the honest cost of the EMI. Compare it to the cash price. The decision becomes mechanical.

When no-cost EMI is genuinely the right choice?

We are not arguing against the product. There are three situations in which it is the right call.

When the purchase is genuinely necessary, and a lump-sum payment would deplete the emergency fund. Liquidity preservation has value. Paying a small premium to keep ₹60,000 of emergency cash available is often the right trade.

When the realistic alternative is a credit-card revolve. If you would otherwise leave the purchase on a credit card and pay only the minimum due, the no-cost EMI at an effective annualised cost in the low double digits is dramatically cheaper than a 36-42% revolve.

When the seller's cash discount on the product is actually small or zero. Some sellers price the cash and the EMI similarly, especially during festival sales where the brand absorbs the financing cost. In those cases, the no-cost EMI is genuinely close to costless. The only way to know is to check the cash price.

When it is the wrong choice?

Three situations to walk away.

When you would not buy the product at the cash price. This is the most important filter. The EMI structure is designed to lower the perceived price of the purchase decision. If you would not pay ₹62,000 in cash for the phone, you should not be paying ₹62,000 on EMI for it either. The decision is the same decision; the EMI is just slower.

When you already have a credit-card outstanding being revolved. Adding another large block of credit on a card whose outstanding is not being cleared turns a manageable situation into a credit-score event.

When a major loan application is planned in the next six months. Home loan, car loan, education loan - these are repriced by the new lender on the basis of your current credit score. A utilisation-driven score hit at the wrong moment is more expensive than the entire EMI saving in the first place.

A practical checklist for the next purchase

The next time you reach a checkout page with a no-cost EMI option, run this in under sixty seconds.

Open the same product in a private tab. Note the cash price.

Add the EMI price + processing fee + GST on the financing component. Subtract the cash price. That number is the premium.

Check your credit-card limit and current outstanding. If this purchase pushes utilisation above 50%, pause.

Ask yourself, would I buy this at the cash price? If no, walk away regardless of the EMI option.

If yes to (4), and the premium in (2) is under 5% of the cash price, and the utilisation check in (3) is comfortable- tap with full awareness.

The checklist is what separates the borrower who used no-cost EMI well from the one who discovered, four months later, that they were paying for a convenience they did not need at a price they did not see.

The bottom line. No-cost EMI is a clever, well-designed Indian consumer-finance product. It is not free- the RBI said so explicitly in 2013, and the underlying principle has not changed. It is also not predatory. It is a structured premium charged to buyers who do not check the cash price. The single sixty-second habit of opening the same product in a private tab before tapping checkout ,that one habit captures most of what is recoverable from the trade.

This article is for educational purposes only and does not constitute financial, legal, tax or investment advice. Specific facts vary by case. For credit and loan-related decisions, work directly with an RBI-regulated lender or an RBI-recognised credit counsellor. For investment decisions, consult a SEBI-registered investment adviser. For insurance decisions, consult an IRDAI-registered intermediary. Statutes, RBI circulars and survey data referenced are accurate as of June 2026 and may be amended or superseded later- always verify with the primary source before acting.